All Categories

Featured

Table of Contents

Right here's exactly how the 2 contrast. The essential difference: MPI insurance coverage pays off the continuing to be equilibrium on your home loan, whereas life insurance coverage provides your beneficiaries a fatality advantage that can be used for any objective (life insurance for new homeowners).

The majority of plans have an optimum limit on the dimension of the home mortgage balance that can be guaranteed. This maximum quantity will be clarified when you make an application for your Mortgage Life Insurance Policy, and will certainly be recorded in your certification of insurance coverage. Yet also if your starting mortgage equilibrium is greater than the maximum limitation, you can still guarantee it approximately that limitation.

They also like the fact that the earnings of her home loan life insurance policy will go directly to pay the home mortgage equilibrium instead of potentially being made use of to pay other debts. term life insurance for mortgage. It is necessary to Anne-Sophie that her family will have the ability to proceed staying in their family home, without financial discomfort

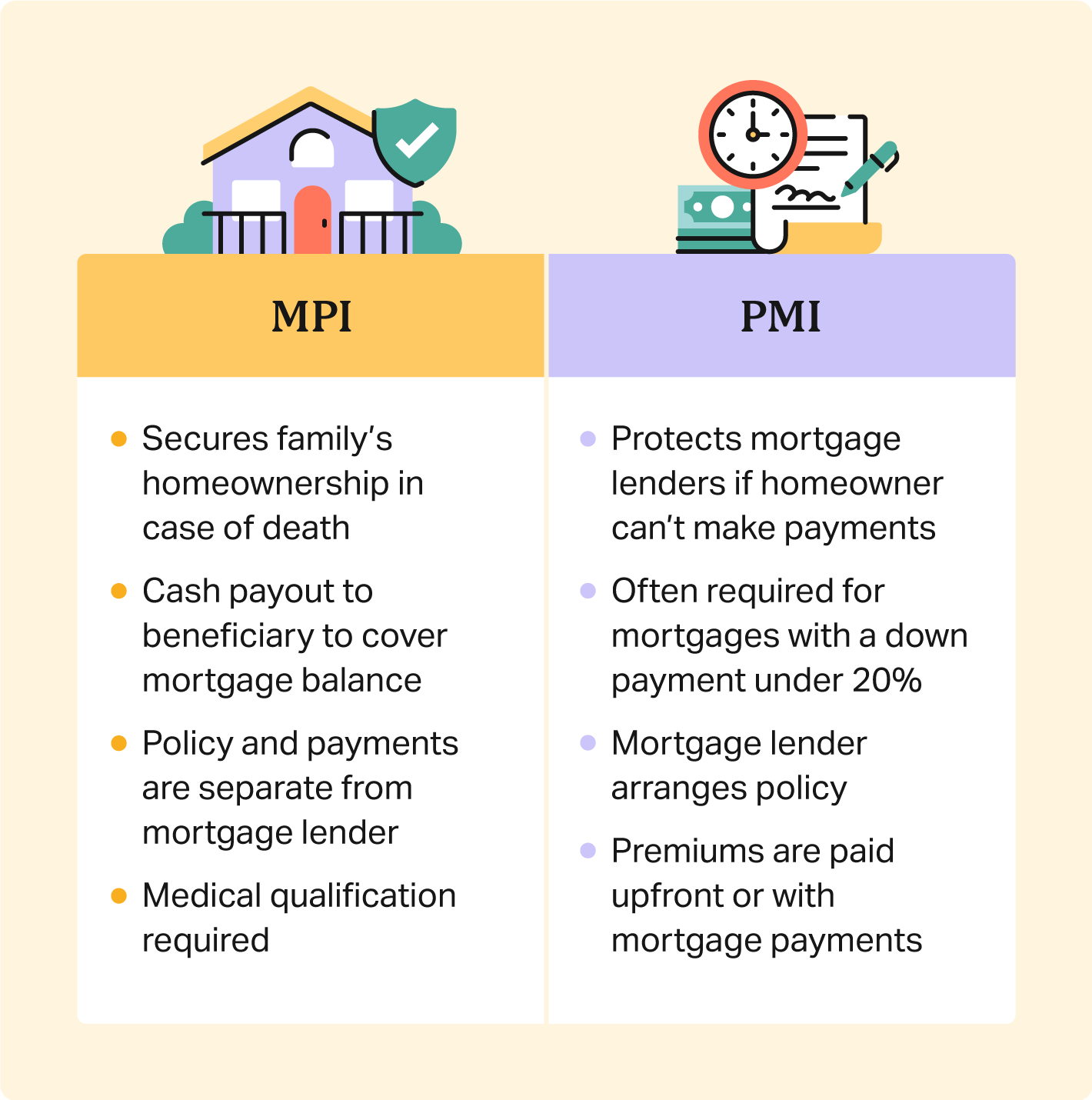

Nonetheless, keeping all of these phrases and insurance coverage types straight can be a headache. The adhering to table puts them side-by-side so you can promptly distinguish among them if you obtain perplexed. Another insurance policy coverage type that can pay off your home loan if you die is a common life insurance policy.

Mortgage Protection Sales

A is in place for a set number of years, such as 10, 20 or 30 years, and pays your beneficiaries if you were to pass away throughout that term. A gives coverage for your whole life span and pays out when you pass away.

One common guideline is to intend for a life insurance policy policy that will certainly pay as much as 10 times the policyholder's wage amount. You might choose to utilize something like the Penny technique, which adds a family members's financial debt, income, mortgage and education costs to calculate just how much life insurance policy is required.

There's a reason new home owners' mail boxes are frequently bombarded with "Last Chance!" and "Urgent! Activity Needed!" letters from mortgage security insurance firms: Many only permit you to acquire MPI within 24 months of closing on your home loan. It's likewise worth noting that there are age-related restrictions and thresholds imposed by almost all insurance firms, that usually will not give older purchasers as several options, will certainly bill them more or might deny them outright.

Rules For Mortgage Insurance

Below's exactly how mortgage defense insurance measures up versus typical life insurance policy. If you're able to qualify for term life insurance, you should avoid mortgage defense insurance (MPI).

In those situations, MPI can give excellent comfort. Simply be certain to comparison-shop and check out every one of the great print before registering for any type of plan. Every home mortgage defense alternative will certainly have various guidelines, regulations, benefit choices and drawbacks that need to be considered carefully versus your exact scenario.

A life insurance policy plan can aid settle your home's home loan if you were to pass away. It's one of many ways that life insurance may aid safeguard your loved ones and their financial future. One of the very best means to factor your home mortgage into your life insurance demand is to talk with your insurance representative.

Rather than a one-size-fits-all life insurance policy, American Domesticity Insurance provider provides plans that can be made particularly to satisfy your family's demands. Here are several of your alternatives: A term life insurance coverage plan (life insurance ireland mortgage) is energetic for a specific amount of time and normally provides a bigger amount of insurance coverage at a lower cost than a long-term plan

Instead than only covering an established number of years, it can cover you for your entire life. It also has living benefits, such as money worth build-up. * American Family Life Insurance policy Company uses different life insurance coverage policies.

Your agent is a terrific source to answer your concerns. They may likewise be able to help you discover spaces in your life insurance protection or new means to minimize your other insurance policy policies. ***Yes. A life insurance policy beneficiary can choose to make use of the death advantage for anything. It's a fantastic way to assist protect the economic future of your family if you were to pass away.

Do You Need Life Insurance When You Get A Mortgage

Life insurance policy is one way of assisting your family members in settling a mortgage if you were to pass away prior to the home mortgage is entirely paid back. No. Life insurance is not required, but it can be a vital component of helping make certain your loved ones are economically safeguarded. Life insurance policy proceeds might be used to aid pay off a home mortgage, but it is not the like home loan insurance coverage that you may be needed to have as a problem of a financing.

Life insurance policy might aid ensure your residence stays in your family members by giving a fatality benefit that might assist pay down a home mortgage or make essential acquisitions if you were to pass away. This is a quick summary of insurance coverage and is subject to policy and/or rider terms and problems, which may vary by state - mortgage and home insurance.

House And Mortgage Insurance

Words lifetime, lifelong and irreversible are subject to plan terms and problems. * Any type of lendings taken from your life insurance plan will accrue passion. Any exceptional lending equilibrium (car loan plus passion) will certainly be subtracted from the survivor benefit at the time of claim or from the money value at the time of abandonment.

** Topic to plan terms and problems. ***Price cuts may differ by state and business underwriting the car or property owners policy. Discount rates might not use to all insurance coverages on a car or house owners plan. Price cuts do not put on the life policy. Plan Types: ICC18-33 (10 ), ICC18-33 (15 ), ICC18-34 (20 ), ICC18-35 (30 ), L-33 (10 )(ND), L-33 (15 )(ND), L-34 (20 )(ND), L-35 (30 )(ND), L-33 (10 )(SD), L-33 (15 )(SD), L-34 (20 )(SD), L-35 (30 )(SD), ICC18-36 (10 ), ICC18-36 (15 ), ICC18-36 (20 ), ICC18-36 (30 ), L-36 (10 )(ND), L-36 (15 )(ND), L-36 (20 )(ND), L-36 (30 )(ND), L-36 (10 )(SD), L-36 (15 )(SD), L-36 (20 )(SD), L-36 (30 )(SD), ICC17-225 WL, L-225 (ND) WL, L-225 WL, ICC17-227 WL, L-227 (ND) WL, L-227 WL, ICC17-223 WL, L-223 (ND) WL, L-223 WL, ICC17-224 WL, L-224 (ND) WL, L-224 WL, ICC17-228 WL, L-228 (ND) WL, L-228 WL, ICC21, L141, MS 01 22, L141, ND 02 22, L141, SD 02 22.

Home mortgage security insurance coverage (MPI) is a different kind of protect that can be helpful if you're incapable to repay your home loan. While that added security seems excellent, MPI isn't for everyone. Below's when home loan defense insurance policy is worth it. Mortgage defense insurance is an insurance policy that repays the rest of your mortgage if you die or if you become disabled and can't function.

Both PMI and MIP are needed insurance policy protections. The amount you'll pay for mortgage security insurance policy depends on a range of variables, including the insurance firm and the current balance of your home loan. how much is mortgage protection.

Still, there are benefits and drawbacks: Most MPI policies are issued on a "guaranteed acceptance" basis. That can be beneficial if you have a wellness problem and pay high prices forever insurance policy or battle to get coverage. An MPI policy can give you and your family members with a complacency.

Life Insurance For Home Mortgage

You can select whether you require home loan security insurance policy and for exactly how long you require it. You may desire your mortgage defense insurance coverage term to be close in size to just how long you have left to pay off your home loan You can cancel a home loan defense insurance plan.

{kind=link}

Table of Contents

Latest Posts

High Risk Burial Insurance

Aarp Burial Insurance Quotes

Final Expense Agents

More

Latest Posts

High Risk Burial Insurance

Aarp Burial Insurance Quotes

Final Expense Agents